As expected, the Federal Open Market Committee kept rates as is yesterday. The effective federal funds rate remains at 0.40%. So now what? If the Fed refuses to raise rates in a time of sustained full employment, rising sticky inflation including real estate prices, and a generally booming economy, what will?

As we’ve said before, only obvious price inflation, which could lead to a dollar crisis, is likely to get them to raise rates to any historically normal level. The problem is, if this is the only thing short of a huge burst in GDP growth to the tune of 5% to get them to raise rates, then, we know almost by deductive necessity that the next time rates are raised, it will only be because of dollar weakness or a dollar crisis, not economic strength. See the PowerShares DB US Dollar Index Bullish (NYSEARCA:UUP) for a good proxy of the dollar index.

The Fed is asking for trouble. By pinning any rate hike on obvious inflation, they are essentially admitting that when they do raise rates, they will be forced to do so due to the currency markets and a possible dollar crisis. That puts the dollar in a very precarious scenario where small, reluctant rate hikes will fail to stem the inflation tide, which could then become exacerbated and necessitate even more aggressive rate hikes.

If the Fed ends up getting more aggressive in an attempt to chase inflation, it would become immediately obvious to traders and they could all end up dumping the dollar at the same time. This would in turn start a positive feedback loop of the Fed raising rates still further to the point of seriously jeopardizing the solvency of the US government, which would buckle the bond market. See the Vanguard Total Bond Market ETF (NYSEARCA:BND) for a good proxy of conditions there.

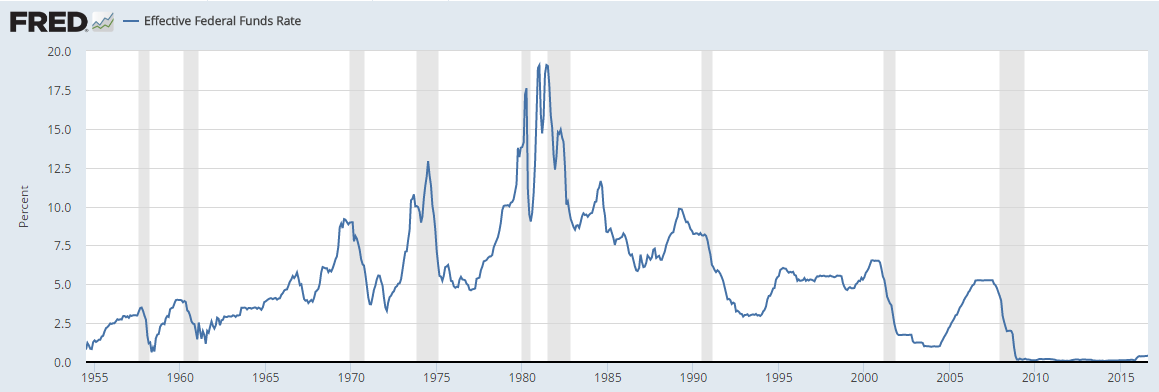

Sound unlikely? So unlikely that it’s never happened before? Something out of the Twilight Zone? Except that it has happened before, from 1978 to 1981.

Why did the effective Federal Funds rate rise from 5% in 1978 to nearly 20% in 1981? Perhaps because the Fed was so enthralled with the spectacular economic growth in those years and the overheated economy that it decided that the economy could handle 20% interest rates on the shortest overnight end of the yield curve?

No, then Fed Chair Paul Volcker decided he had no choice and raised overnight rates to astronomical levels in order to save the dollar, which was experiencing 15% annual inflation at the time. Volcker had no choice but to jump in front of that with even higher rates of 20%.

By refraining from raising rates now when the economic situation is rather decent, the Fed is asking to be tested by dollar weakness. If and when it comes, they will raise rates by a quarter point, but that won’t be enough. They’ll be forced to chase inflation with higher and higher interest rates just as Volcker did before being replaced by Alan Greenspan.

However, current public debt levels make doing that kind of thing – raising rates to 20% – quite impossible without destroying the bond market and forcing a default on US Treasuries. The clock is ticking and the Fed is running out of time, but they don’t even realize it. They believe they will be able to slowly and gradually raise rates, but have no plan for what to do if inflation really gets out of hand. By the time inflation becomes obvious it may be too late to do anything.

All the ingredients for a positive feedback loop are already in place. All that is needed now is a spark. What is the magic number that will get it started? This is just a guess, but an official government-measured inflation rate of 3% to 5% should be enough to get the Fed to start chasing with rate hikes. Except that the Fed is chained to the bond market, and when it starts chasing inflation, the bond market could become completely uprooted.

Intercept Pharmaceuticals (NASDAQ:ICPT) Gilead Sciences, Inc (NASDAQ:GILD) Clovis Oncology, Inc. (NASDAQ:CLVS) Chiasma, Inc. (NASDAQ:CHMA)")

Might Be Moving Away From Its Initial Plan With Messenger")

Is Running Right Now")