, Immunomedics Inc (NASDAQ:IMMU), BioMarin Pharmaceutical Inc (NASDAQ:BMRN), Cara Therapeutics Inc (NASDAQ:CARA)")

Since we already covered Sarepta Pharaceuticals (NASDQ:SRPT) and Collegium Pharmaceuticals (NASDAQ:COLL) last week with FDA panel reviews due today and tomorrow, this week we will review some more minor developments that occurred last week in biotech and their implications for the future. Let’s begin with Sucampo.

Sucampo Pharmaceuticals

On April 19th, Sucampo Pharmaceuticals announced disappointing news for its candidate cobiprostone for the treatment of non-erosive reflux disease (NERD) and symptomatic gastroesophageal reflux disease (sGERD). These two indications are more commonly known as heartburn, or acid reflux. Cobiprostone did not meet the primary endpoint of a Phase IIa trial designed to show clinical benefit by symptomatic scores. In other words, the patients taking the drug did not feel any better after taking it. Sucampo decided that it was ending the development of cobiprostone for these indications, but that it would continue developing the drug for oral mucositis.

There is a lot of missing information surrounding this failure that raises concerns about the company from the perspective of its cobiprostone pipeline. On the one hand, Sucampo’s lifeline is not cobiprostone, but its flagship drug lubiprostone, or AMITIZA for the treatment of constipation of various forms. AMITIZA sales are flying high, the drug works, the company has a plan for expanding its market, a new partnership with a Chinese pharmaceutical company will soon open up that market as well, and a trial testing AMITIZA on teenage patients looks very promising. All that is the reason that Sucampo shares were not affected for more than a day after this news was released. The failure only takes down potential value and has nothing to do with the company’s success with AMITIZA.

On the other hand, we believe Sucampo will suffer from more bad news with cobiprostone in the future. Part of Sucampo’s quick recovery may have been inherent in the assumption that cobiprostone would succeed in the oral mucositis indication. The chances of that are not very good in our opinion, though I can’t put a number on it because so much data is missing. We’ll get into that in the sections below.

The Science

Cobiprostone is a prostone, a type of molecule found naturally in the human body that triggers ion channels in cell walls by either activating them or closing them to ion transport. Ions are charged particles whose concentrations in and out of cells affect the flow of water in and out of cells. This is the concept on which AMITIZA is based. Lubiprostone, short for lubricating prostone, activates chloride ion channels in the intestine which causes chloride to leave and water to enter. This makes the stool more watery, which is beneficial for those suffering from constipation obviously. Different prostone molecules are targeted to different cells, so they can be targeted to specific locations, and cobiprostone targets the neck and mouth area while lubiprostone targets the intestine. That cobiprostone works similarly to lubiprostone is evident in the most commonly reported side effect in the failed trial, being mild diarrhea.

The theory was that cobiprostone would selectively activate chloride ion channels in the esophagus, which would stimulate the production of mucus there, protecting the esophageal cells from getting burned by stomach acid. The concerning thing about cobiprostone is not necessarily that it failed, but that Sucampo is being a bit tight-lipped as to why.

The Data

The only piece of evidence we have regarding the efficacy of cobiprostone is the press release from April 19th. There we learned that “cobiprostone demonstrated significant benefit in some of the secondary measures of this exploratory study” but there is no word on what these secondary measures are. Mucus buildup perhaps? The problem is that not only is Sucampo not specific, but there is no record of the trial on Clinicaltrials.gov to even find out what the secondary endpoints were. All we know is that it was a 14-week placebo-controlled 140-patient trial.

The reason this is important is that knowing what exactly cobiprostone did achieve, if not its primary endpoint, would give investors a hint as to its chances of success in the oral mucositis indication. If, for example, we knew that cobiprostone did in fact increase mucus protection in the esophagus, just that doing so did not help symptoms as expected, we could then take that as evidences that there is a better chance cobiprostone would work on oral mucositis patients. But we don’t know as of right now.

Investors and those interested in holding Sucampo shares should pay close attention to the upcoming earnings call scheduled for Wednesday, May 4th at 8:30am. Hopefully management will address what exactly happened at this trial, give possible reasons why it failed, and more importantly where exactly it succeeded. If these issues are not addressed directly, hopefully they will be in the question and answer session.

The Market

According to Sucampo, the potential market for the NERD/sGERD indication for cobiprostone was 8 million patients. Though the NERD/sGERD population is much bigger, prescription acid inhibitors do work for much of the population and over the counter drugs for others, so Sucampo was targeting a patient population for whom inhibiting acid production does not work. That market is now out the window.

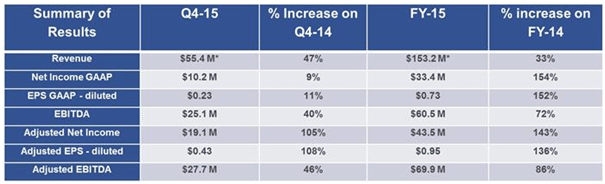

If we assume similar pricing for cobiprostone as for AMITIZA, the numbers are as follows. Total AMITIZA prescriptions for 2015 were 1,475,634 with total revenue at $153.2 million. That’s about $103 of revenue per prescription filled, which would have put the cobiprostone addressable market at $830 million a year ultimately. It would have taken some time to reach that number obviously, but it looks like it would have more than doubled Sucampo’s value from a fundamental standpoint. Not to be.

The Reaction

The market reaction to this phase 2 failure was silly but expected. Sucampo is a growing company with a successful first product that looks set to expand much farther in the near future. Here is a growth table from one of its investor presentations.

Shares initially dropped 20% on the news but recovered completely the next day. A 20% fall for a company growing this nicely does not make sense, and was probably due to retail traders or dumb money that reacted instinctively to sell at market on bad news. Good news should have certainly caused he stock to rise significantly if temporarily, but the heartburn indications were really a bonus shot for Sucampo rather than its bread and butter.

The deeper question is what was the main factor in causing the stock to recover so quickly. To the degree that it was due to investors hoping that the oral mucositis indication would be more successful, is bad news. If it was mostly based on the expanding market for AMITIZA, that’s good news.

If investors bought back shares hoping for success in oral mucositis, they are not very likely to get it, in our opinion. Oral mucositis is a disease that sufferers of head and neck cancer get as a result of chemotheraphy or radiation to that area of the body. The cancer treatment kills mucosal cells that reproduce very fast like cancer cells, which is why they are attacked by the treatment. There are two primary reasons we don’t see cobiprostone succeeding with this indication. First, if cobiprostone really did help mucus production in the failed study, which is not specified, then it would have said this explicitly in the press release to give hope to those banking on this indication. But even if it did, and it may very well have, optimizing cells not producing enough mucus is very different from causing cells battered by chemotherapy and radiation to produce mucus.

In other words, even if cobiprostone caused cells in the lining of the esophagus to produce more mucus, those cells are still essentially healthy. The malfunctioning and dying cells in the oral mucositis case are not healthy by any means, and it is doubtful if a chloride channel opener can suddenly make them work again when they are being attacked from all directions by cancer treatment.

The potential market for oral mucositis is about 30,000 annually in the US. This is extrapolated from head and neck cancer figures against those sufferers treated with aggressive chemotherapy and/or radiation that causes oral mucositis.

Finances

The table above gives a good idea of the improving finances of Sucampo despite this failure. Since it is profitable it is no longer a development stage company and has no pressing cash clock counting down the time to a needed approval. The Chinese deal with AMITIZA and the development of the Chinese market for that drug is what to watch on the financial front. The deal was signed in May and marketing depends on approval from the China Food and Drug Administration. Approval looks probable if not assured, since AMITIZA is marketed in both Europe and the US already. The trial appears to be a formality, but acceptance of the drug in the Chinese market would be huge for Sucampo, much more important than the oral mucositis indication which looks more far-fetched.

Valuation and Trading Strategy

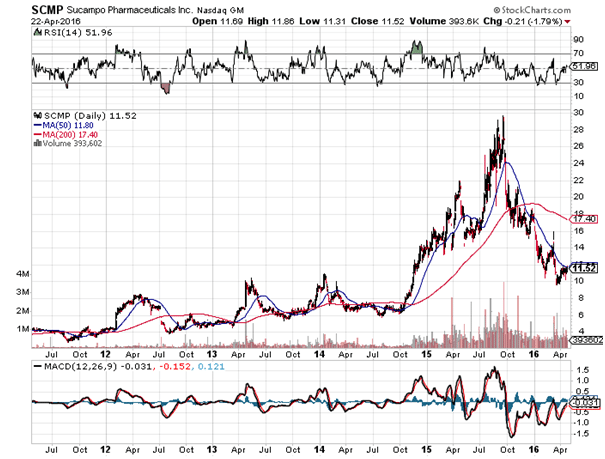

Sucampo shares have collapsed 62% since biotech topped in mid 2015. Fundamentally though, the company is succeeding nicely. Price to earnings is only 15.8, low for a young and succeeding biotech firm. AMITIZA will probably be approved for the teenage constipation market eventually, as well as for the general Chinese market. Finances will continue to improve as the US and European markets grow and the drug becomes more popular. A viable strategy would be to go long here with 70% of your ultimately desired position, and then to complete the rest after the release of the oral mucositis results around December, which I expect will not be good.

If results are negative, it should give another good entry point, but most of the position should be taken now in case results for oral mucositis are unexpectedly positive, along with the fact that biotech in general is continuing a nice recovery.

Immunomedics

Last week on April 18th, Immunomedics, Inc. announced positive Phase II results for labetuzumab govitecan, an antibody drug conjugate (ADC) for the treatment of metastatic colorectal cancer.

The Science

Antibody drug conjugates are simply cytotoxic drugs attached to an antibody designed to function as a homing mechanism. The antibody attaches to a cancer cell, releasing the drug to kill the tumor. The unique thing about labetuzumab govitecan is that Immunomedics has a slightly different theory with regard to ADC efficacy than other companies who develop similar medications. The difference is that most companies go after the most toxic drugs available to attach to antibodies on the theory that the homing device will prevent the drug from acting anywhere else in the body, so one may as well use the more toxic drugs.

Immunomedics believes that this approach is flawed, and that it is better to attach only moderately toxic drugs to antibodies but instead load more of that drug to the antibody, allowing for repeated dosing. Its drug of choice is SN-38, a metabolite of an already approved chemotherapy. For its flagship candidate, which is not the one that just reported Phase II results, the average ratio of SN-38 to antibody on Immunomedics ADC’s is 7.6:1. Preclinical studies showed that delivery of SN-38 to the targeted tumor is increased 135-fold when compared to the standard chemotherapeutic delivery.

Labetuzumab govitecan has the same active ingredient SN-38 with a different homing mechanism that locks on to carcinembryonic antigen, expressed in 90% of all colorectal cancers.

The Data

The Phase II study tested 82 patients, 75 of whom reported side effects. 15% reported neutropenia, 7% diarrhea, and 3% febrile neutropenia, all considered grades 3 and 4 adverse events. Median progression-free survival and overall survival were 3.9 and 6.7 months, respectively. Immunomedics thinks this is a good sign because a different drug, regorafenib, was approved based on a median PFS of 2 months and median OS of 6.4 months. So far, lebtuzumab govitecan is better.

The key being, so far. Regorafenib, sold as Stivarga, was approved based on a trial of 760 patients. This trial was only 82 patients, so the data might change significantly after a larger phase III trial. Overall survival was the primary endpoint in the Stivarga trial, and came in at 6.4 months over 5 months placebo. In fact, most failed drugs get tripped up when phase II results are not repeated in phase III. So while the data is encouraging, it is not without its caveats.

The Market

The colorectal cancer market is expected to top $9 billion by the end of the decade. Not to get ahead of ourselves though, labetuzumab govitecan is not going to conquer that market even if approved, and we are not even close to that yet. It is not going to be a first line therapy, and while it does seem to increase overall survival, as a salvage therapy patients may not even elect to take it some of the time. By that point many patients are tired living in hospitals and suffering side effects and would rather spend the rest of their time with their families. So it is impossible to tell what the real addressable market is for labetuzumab at this point.

The Reaction

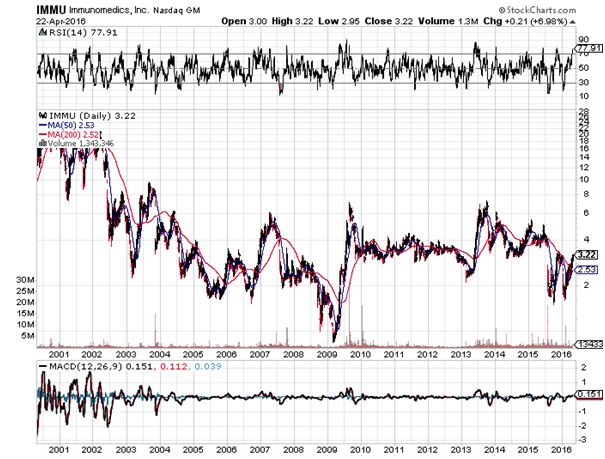

While there was no discernable reaction from the stock on the news, Immunomedics has been in a strong uptrend since the beginning of the year, having climbed 87% since February. This is not the first time that the stock has gained fast in a short period of time. We saw much bigger moves in 2006, 2009, and 2013, none of them sustained. While the company’s flagship candidate is moving to phase III trials, there is still a while to go before there are any results. Clinicaltrials.gov has the primary completion date at 2021.

Any way you look at it, Immunomedics still looks to be years away from any marketable product, and though the recent phase 2 results are encouraging, they should have no bearing on the price nor did they.

Finances

Immunomedics has about $78 million in liquid assets, but luckily they are not funding the huge phase III trial for their primary candidate epratuzumab. Quarterly burn rate is about $14 million which gives the company about a year to a year and a half before it needs to refinance again. It will have to do that eventually and shareholders will most likely get diluted.

Valuation and Trading Strategy

When dealing with companies relatively far away from market, valuation becomes a guessing game. The idea of using a moderately toxic drug for an ADC is unique and may work, but we are too far away to determine that. The stock should be avoided for now because its behavior is notoriously volatile as you can see in the chart above, and is more the territory of institutional investors who take long term stakes in speculative companies. By the time its first candidate gets to market, maybe in 5 years or so, the entire landscape of the cancer space could change dramatically, so this one is really a shot in the dark. It should be certainly followed, but let the big money place bets here. Sucampo is a much more compelling buy than Immunomedics, despite Sucampo reporting the failure and Immunomedics reporting the success this week.

BioMarin Pharmaceutical

![]()

On April 20, 2016 BioMarin Pharmaceutical gave us an update regarding its ongoing phase 3 trial in achondroplasia. Achondroplasia is a type of dwarfism that results in shortened limbs, and it is especially prevalent in children. BioMarin’s candidate is called Vosoritide. There is currently no available treatment for the condition, so if approved, it should quickly become standard of care in the field.

The Science

To understand the drug, we must first look at the condition. In our bodies, we have a receptor called fibroblast growth factor receptor 3 (FGFR3). In healthy patients, when a protein activates this receptor, it results in the controlled down-regulation of chondrocytes, which are the cells responsible for bone and cartilage growth.

In patients with achondroplasia, the receptor is constantly activated, meaning far higher than normal levels of down-regulation. This results in shortened limbs – the common symptom associated with the condition.

Vosoritide is an analog of (just meaning it’s a synthetic version of) a protein called C-type natriuretic peptide (CNP). This protein reduces the effect of the FGFR3 receptor, and in turn, can theoretically be used to treat achondroplasia.

The Data

The company released six-month data a little while back, and demonstrated a 2 cm/year increase in mean annualized growth. The goal of extension was to replicate this data and prove that the drug is effective over an extended period of time. At 12 months, the patients showed a 1.9 cm per year mean annualized growth velocity, so we can consider the release as demonstrating efficacy across the extension period. Further, in patients who went from a lower to a higher dose, growth increased. This is important because it illustrates a more potent efficacy at a higher dose – something that supports the primary endpoint.

The Market

How big is the market for achondroplasia? As we’ve said, there is no current standard of care for this type of condition. Incidence rate on a global scale comes in at about 96,000. The drug is targeting children, which account for about 25% of this total global population. The potential market comes in at around 24,000 individuals globally. Of these, just shy of half are in the US. We don’t yet have a price point for the condition, and comparisons are difficult given its unique nature, but it’s not unreasonable to suggest that BioMarin could charge high double-digit thousands or even low triple digit thousands of dollars for an annual course. In turn, this gives Vosoritide a blockbuster market potential.

The Reaction

In development stage biotechnology, data such as this could easily translate to a 20 or 30% gain in market capitalization. For a company of BioMarin’ssize, however, the drug even if approved would only represent a relatively low percentage of overall revenues. With this in mind, the reaction is often muted. We saw exactly this play out here, with the company only gaining 2% on the positive news.

Finances

In line with what we said in the previous section, BioMarin’s size separates it from many of the companies we cover, in that finances shouldn’t be a problem going forward. During 2015, the company generated $228 million revenues, for a net income of $66 million. Cash on hand, at last count came in at $397 million.

Trading Strategy

There’s no real strategy surrounding this release – that is, until we get a PDUFA on NDA submission. Once we know when the FDA will rule on Vosoritide, we can target some upside on the approval and – conversely – any potential decline on the agency saying no.

Cara Therapeutics

Back in February, we got word that the FDA had placed a clinical hold on Cara Therapeutics lead candidate CR845. The drug is a postoperative pain candidate, and is currently in phase 3 trials across two dose arms and a placebo arm. The hold was rooted in a prespecified stop criterion, based on elevated levels of sodium in blood serum. We’ll take a look at this in a little more detail shortly, but first, here’s a quick look at the science behind the treatment.

The Science

CR845 is an opioid in pain management drug. Currently available opioids act on opioid receptors, part of the central nervous system. The problem with these, however, is that they impact signals sent to, from, and through the blood-brain barrier. This interaction with the brain leads to the commonly associated side effects – nausea, anxiety etc. It’s also the primary driver behind opioid addiction and misuse. Instead of acting upon the receptors in the central nervous system, CR845 targets the periphery system. This is the part of the central nervous system that lay outside of its main structure, and it doesn’t interact with the brain. The drug activates kappa opioid receptors that form the periphery system, and works to alleviate pain (in this instance, post operative pain), without the side effects of current standard of care opioid pain management treatments.

The Data

So what did the release tell us about the drug and the clinical hold? As mentioned, the FDA put a hold on the trial in response to a prespecified element of the trial that relates to increased sodium levels. Treatment centers reported an elevated serum sodium level in patients across the trial, and the FDA initiated a clinical hold while they unblinded these patients to see if the elevated levels related to particular dosage.

As the latest release tells us, serum sodium levels did indeed relate to a specific dosage – in this instance, the 1 ug/kg intravenous administration arm of the trial. Cara announced that with this identification, the FDA has allowed the company to go on with the trial, with no major alterations. That is, maintaining the two dose arms as previously specified as part of the trial outline, alongside a placebo arm, reblinded.

The Market

If approved, what is the market potential for CR845? As said, the drug is a postoperative pain indication. In the US, every year, there are 46 million inpatient and 53 million outpatient surgeries, the vast majority of which require postoperative pain medication. 95% of this medication is opioid based. If Cara can prove efficacy of the ongoing phase 3, it’s not unreasonable to suggest that the company could quickly become a major competitor in the postoperative pain space. Exactly what penetration this infers remains unclear, but a multibillion-dollar market looks achievable. It all depends on comparative efficacy. If CR 845 can prove equivalent to current SOC, or even better, demonstrates a stat-sig improvement over the currently available therapies, the market potential is huge.

Reaction

Market response to the announcement was relatively muted. The company sold off back in February when the FDA imposed the clinical hold, and it’s lifting should really have translated to at least some closing of the downside. As things stand, however, Cara remains down on its April 20 open. Whether this will change come market open this week remains to be seen. As markets digest the lifting of the clinical hold, there’s a good chance we will see some upside.

Finances

With a market capitalization of just $180 million, Cara falls well within the small cap bracket. This means an investment in the company comes with all the associated financial risk we normally address when covering companies of this size. Specifically, the company’s ability to finance trials through to completion is a major risk factor going forward. Cara generates little to no revenues (it’s only revenues recorded come off the back of research grants) and reports a net loss every quarter. During the final quarter of 2015, this net loss came in at $9.5 million. More importantly, the company’s balance sheet reported $15.1 million cash and cash equivalents at last count (December 31, 2015), meaning Cara will almost certainly need to raise capital before it can carry its pipeline through to completion. This raise will likely come through share issue, and in turn, could dilute the holdings of any current or early-stage investors.

Trading Strategy

How can we approach Cara going forward? As noted already, market response to the clinical hold lifting was pretty much nonexistent, meaning markets are likely looking to an interim analysis before forming a bias. Management expects to offer up this interim data before the end of the year, specifically citing third-quarter 2016 as a target period for release. As such, our approach towards this one is a current hold, with a view to gauging the drug’s chances of approval based on phase 3 interim during Q3. If we see equivalence to current SOC, chances are we’ll see some concurrent rise in Cara’s market capitalization before the year draws to a close.

Intercept Pharmaceuticals (NASDAQ:ICPT) Gilead Sciences, Inc (NASDAQ:GILD) Clovis Oncology, Inc. (NASDAQ:CLVS) Chiasma, Inc. (NASDAQ:CHMA)")

Might Be Moving Away From Its Initial Plan With Messenger")

Is Running Right Now")