This article discusses Tesla (Nasdaq:TSLA), Blink Charging (NASDAQOTH:CCGI) and PPG Industries, Inc. (NYSE:PPG).

In 2016, registrations of electric cars hit a new record in 2016, with over 750 thousand sales worldwide. Until 2015, the US accounted for the largest portion of the global electric car stock, however, in 2016, China took the lead, accounting for circa one-third of the global total.

With numerous global political and economic efforts pushing for sustainability, there is a good chance that we will see the US, China and Europe tussle for first, second and third place over the coming two decades.

Which region takes the top spot, however, is relatively insignificant in terms of global demand.

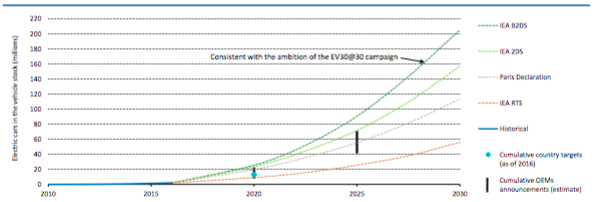

The chart below illustrates global deployment scenarios for the stock of electric cars to 2030.

As illustrated, global stock is expected to increase by close to 10,000% between 2017 and 2030.

Of course, a number of companies are positioned to take advantage of this growth, each of which offers an investor the opportunity to piggyback industry expansion as the electric vehicle revolution takes hold.

Many of these are obvious plays – Tesla Inc (NASDAQ:TSLA), General Motors Company (NYSE:GM), etc.

There remains a number of under the radar companies in the space, however, that very few people are looking at right now but that have the same if not more potential for growth as those mentioned above as we move along the curve illustrated in the chart above.

Here is a look at two of these under the radar plays.

Blink Charging Co(NASDAQOTH: CCGI) (OTCMKTS:CCGI)

First up, Blink.

As the electric vehicle industry expands, drivers are going to need places to charge their vehicles. With its network of superchargers Tesla provides what is essentially coast-to-coast charging access to Tesla drivers but, as things stand, drivers of other electric vehicles are relatively limited in terms of charging locations across the US.

Blink has recognized this opportunity and is working to fill this gap in the market.

The company offers residential and commercial EV charging equipment that enable EV drivers to recharge at various location types. It has strategic partnerships across a wide range of locations, including everything from municipal locations, healthcare/medical facilities, universities, stadiums, supermarkets and more.

At the end of 2016, Blink reported that it had just shy of 14,000 charging stations spread across the US, of which around 5,500 are Level 2 public charging units and 2,377 residential charging units. The majority of the remainder comprises a little over 5,000 non-networked, residential Blink EV charging stations, which are all partner owned.

When you consider that there only exist 16,500 charging stations in the US right now and a little over 45,000 charting outputs, it’s clear that Blink controls a substantial portion of the space and is going to play a key role in providing the network infrastructure required to support this industry as it continues to take off going forward.

One of Blink’s major competitive advantages is its early mover benefit. Some reading might already be familiar with the company and those that are might know it as Car Charging Group, which was the company’s name prior to a rebranding that took place in August 2017. The company has been around for the better part of a decade and has spent this time building out its network in anticipation of the industry taking hold and expanding. Many argued across this period that the company was jumping the gun but, as current levels of industry growth demonstrate, getting in ahead of all of its competitors has put Blink in a position of first mover strength.

The company is also positioned to take advantage of numerous US government schemes, including the release up to $4.5 billion in loan guarantees and the government’s invitation for applications to support the deployment of commercial EV charging facilities (from July 2016) and the launch the Fixing America’s Surface Transportation (FAST) Act (an Obama-era policy), which was put in place to identify and develop corridors for zero emission and alternative fuel vehicles, which will include a network of EV fast-charging stations.

From a fundamental perspective, the company’s latest numbers derive from the third quarter of 2017.

Charging service revenue from company-owned charging stations came in at $328,000 for the period, up 3% on the same quarter during 2016. Network fee revenue increased 29% across the same period, while total operating expenses decreased by 34%, from $2.33 million during the third quarter of 2016 to $1.53 million for the same quarter in 2017.

Gross profit increased more than 550% between the two quarters in question, from $54,000 to more than $301,000 respectively.

The fact that the company is able to increase its revenues while reducing operating expenses and improving margins is testament to its strong foothold in this growing sector.

PPG Industries, Inc. (NYSE:PPG)

It’s perhaps a bit misleading to call this one an under the radar play – PPG is a $30 billion chemicals and coatings behemoth that’s currently trading at all-time highs in and around $120 a share.

With that said, however, very few people looked at it as a potential electric vehicle stock until very recently, when a couple of fresh announcements hit press at the end of last year and into early 2018.

The first of these came on November 17, when PPG announced that it had entered into a partnership with a company called SiNode Systems. The partnership is set up to “to accelerate the commercialization of high-energy anode materials for advanced battery applications in electric vehicles.”

So what does this mean?

Back in 2016, SiNode was selected among several competitors to receive a contract for the project from the United States Advanced Battery Consortium LLC (USABC). As part of the contract, the US government provides 50% of the funding, while project partners fund the remaining 50%.

We don’t really need to going to the technology side of things here but basically, the product that SiNode has developed is a technology that allows for a reduced battery weight while also improving the range offered by the battery in question. PPG will source and provide graphene – a nanoscale-thin layer of pure carbon that is required for the high-energy anode materials – and prepare the material for SiNode, which will then apply it to its battery technology.

But that’s not all.

On January 3, 2018, PPG announced that its management would discuss the use of its coating technology in electric vehicles and, specifically, as relates to the batteries of these vehicles, at the North American International Auto Show (NAIAS).

This event took place on January 17 and the primary focus of the discussion was rooted in a coating technology for electric vehicle batteries that allows the batteries to maintain insulation from the intense heat they create and, in turn, to reduce or negate the potential for fire or other heat-related activity issues.

For anyone looking to pick up a bit more insight into this technology, it’s covered in detail as part of this presentation.

PPG is already the number one OEM provider globally in the automotive industry, meaning the company should have no problem achieving a substantial market share as EV grows, simply by integrating its coating technology into its existing operational chain.

Again to touch on the fundamentals, PPG just reported fourth-quarter financials, with revenues during the quarter reaching $3.68 billion and net loss coming in at $184 million.

Cash on hand at the end of 2017 was $1.43 billion and the company expects to deploy at least $2.4 billion of cash in 2018 backed by acquisitions and share repurchases.

Two Different Exposures, One Growing Industry

While both of these companies remain under the radar in the electric vehicle space right now, each offers an entirely different allocation type to an investor looking to pick up an exposure to the coming industry growth.

Blink is a small company and, with that, comes an increased degree of risk, but it’s a far more direct exposure and has a far higher potential upside if it is able to leverage its current positioning and grow with the wider electric vehicle market between now and 2030.

PPG, on the other hand, is a much more diversified company with a lower risk profile but, while it stands to benefit from its exposure to electric vehicles and, specifically, electric vehicle battery coatings, the portion of overall sales that its electric vehicle operations will account for, even against the backdrop of a high growth industry, is much smaller as a representation of the company as a whole than is the case for Blink.

Intercept Pharmaceuticals (NASDAQ:ICPT) Gilead Sciences, Inc (NASDAQ:GILD) Clovis Oncology, Inc. (NASDAQ:CLVS) Chiasma, Inc. (NASDAQ:CHMA)")

Might Be Moving Away From Its Initial Plan With Messenger")

Is Running Right Now")