The Federal Reserve Bank of Atlanta routinely publishes a special inflation index known as the Sticky-Price CPI. Generally speaking, it is a measure of the prices for goods and services that don’t usually experience wild swings. In other words, when the prices for these things rise, it usually takes a significant amount of time for them to come back down, and the same for when they fall.

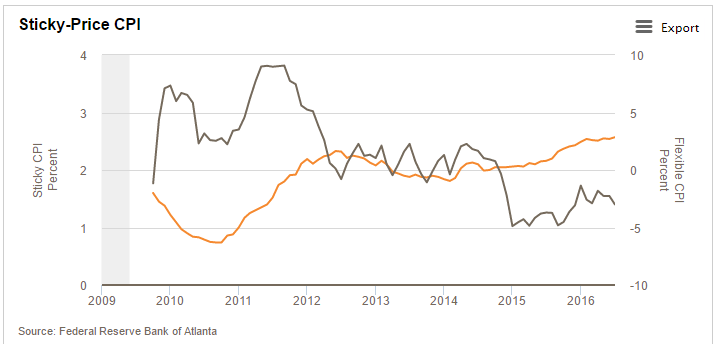

Right now, the Sticky-Price CPI is at its highest level since April 2009, which was officially part of the last recession. This has big implications for gold and the SPDR Gold Trust (ETF) (NYSEARCA:GLD) and especially gold mining stocks, because gold tends to rise quickly when fears of inflation become mainstream. Right now inflation expectations are quite subdued particularly because the more flexible CPI is actually negative.

As you can see from the chart above, the sticky CPI has been trending up consistently since 2009. The flexible CPI, on the other hand, has been negative since October 2014. This was around the time when oil prices began to plummet in a price war between OPEC and nascent energy companies in the United States.

For two years then, flexible prices have been declining, and still the inflation rate has been consistently above zero since that time. This is remarkable in itself, and speaks of the strength of the price increases in the sticky CPI. These principally include recreation, medical care, real estate, food away from home and furniture.

In addition to that, the money supply in the US looks to be on a major upswing. The one-week average M2 supply is on the verge of breaking $13 trillion for the first time in history with no signs of stopping. This is 38% higher than 5 years ago in September 2011 when gold hit a peak of over $1,900 an ounce. With 38% more money in the banking system now and the gold price still 30% lower than that peak, the effect of obvious inflation on the price of gold, when it comes, could be extreme.

Currently, the average Joe on the street has little idea of what the price of gold is because he does not fear inflation. He expects his dollars to more or less retain their value, or that their value will decline slow enough that he will not notice it or that he will get pay raises to compensate. If he loses these expectations, the average person will start turning to gold.

Right now the metal is only an investment hedge for institutional players, and still trending up since December. If inflation starts to become obvious though, and the sticky CPI suggests that this might soon happen, any upside revaluation in the price of gold is likely to be quick and intense.

Disclosure: At the time of writing the author was long gold and gold equities.

Intercept Pharmaceuticals (NASDAQ:ICPT) Gilead Sciences, Inc (NASDAQ:GILD) Clovis Oncology, Inc. (NASDAQ:CLVS) Chiasma, Inc. (NASDAQ:CHMA)")

Might Be Moving Away From Its Initial Plan With Messenger")

Is Running Right Now")