There are a few names in every sector that develop a reputation on the back of repeated investment success. Sometimes these investors are passive in just taking a position and letting it play out. Sometimes they are active, buying up a portion of a company and through various degrees of involvement try to steer that company towards success. Active or passive, those investors that develop this type of reputation accrue a following – a group of retail investors that seek to replicate the positions of the bigger names. This adds to their success as other traders mirror and amplify their moves.

In the biotech sector, and especially in the small cap spectrum of the space, there is no bigger name than Dr. Philip Frost. Across a career spanning the last half century, Frost has built a net worth over a billion dollars, the vast majority of which derives from founding, buying, selling and investing in biotechnology entities.

When Frost takes a position in a small cap biotechnology company, a hoard of individual retail investors sits up and takes notice, and this will often be enough in itself to inject a degree of short term upside momentum into the stock.

On February 8 a company called Polarityte Inc (NASDAQ:COOL) filed this 13G with the SEC detailing a 9.99% stake held by Frost. The filing was an amendment of a previously filed disclosure rooted in an acquisition and a name change for the company. The company used to be called Majesco, and was a video game publisher in which Frost held a 10% position. A video game company by description, but as per Frost’s often-used modus operandi in these sorts of situations, it was for all intents and purposes a shell through which Frost was looking to offer a promising private entity a route to the public markets and – by proxy – access to public capital.

In December, news hit that this strategy had taken effect here, and that Majesco was to merge with a company called PolarityTE, with the latter becoming a wholly owned subsidiary of the former, but with the new entity taking the name of the latter. This sort of arrangement is something we’ve seen numerous times in the past with Frost, with companies including CoCrystal Pharma Inc. (OTCBB:COCP), SciVac now VBI Vaccines, Inc. (NASDAQ:VBIV), and Plumatrix Inc. (NASDAQ:PULM) among others. Other times he takes stakes indirectly through his main company Opko Health Inc. (NASDAQ:OPK). Whichever way he does it, when he is the instigator as is looking like the case here, it always warrants a closer look.

In this instance, however, it’s not just Frost that makes it interesting.

There are also a couple of other big names attached to the stock that serve to reinforce the suggestion that there’s value in this newly combined entity. One is Rob McEwen, founder and former chairman of Goldcorp Inc. (USA) (NYSE:GG). With him at the helm, Goldcorp grew from a $50 million microcap to a $20 billion industry giant. Through an entity called Ontario, Inc., of which McEwen is the current President, he owns 60,000 shares.

The other is Michael Serruya. Alongside his brother Aaron, Serruya amassed a more than $300 million fortune in the fast food and drink space, with the most notable recent transaction being the sale of Kahala Brands, a food service brands franchisor, including Cold Stone Creamery and Blimpie, to MTY Food Group Inc (TSE:MTY), for around $320 million in cash and stock. Serruya’s current stake amounts to 33,334 shares (page 55).

So we’ve got a company here that is essentially brand new to public markets, and that has a current market cap of just $20 million, but which has three high net worth backers commanding various positions in it. As mentioned above, the combined involvement of Frost, Serruya and McEwen will be enough to draw a considerable amount of speculative buy volume to a company of this size, and we’re already seeing this volume affect price – the company is up close to 50% year to date.

But it’s not enough just to have big names. What do these three see in the company?

PolarityTE was founded by Dr. Denver Lough, a surgeon who specializes in regenerative medicine and reconstructive surgery, and who has become the CEO of the post-merger entity, taking over the position from Barry Honig, one of Frost’s long time deputies.

As per Lough’s specialty, the focus of the new company is regenerative medicine, and it’s rooted in a technology called SkinTE. Before looking at that in more deatil, let’s kick things off with a quick introduction to the space. It’s tissue engineering, rooted in wound care and recovery management. The current wound care market is essentially stagnant, and a throng of old and relatively ineffective products are currently in widespread use. To date, no form of autologous tissue engineering is in use, and the importance of this will become clear when we get to SkinTE. The global market for tissue engineering and regeneration is expected to grow to $56.9 billion by 2019, with a five-year compound annual growth rate (CAGR) of 22.3%. Of this growth, stem cell technologies represent the largest and fastest growing category with a significant CAGR of 26.2%. North America will represent $22.8 billion of the market, while the Asia-Pacific region will account for just shy of $10 billion.

It’s a big market, in need of a shakeup.

So how does PolarityTE intend to cause this shakeup? Through SkinTE, PolarityTE is able to regenerate full-thickness, fully functional skin. It’s an off-the-shelf system and at concept level, it’s remarkably simple. The company takes a sample of the patient’s skin via biopsy, and then imprints the cells in a laboratory setting into a 3D system using SkinTE. The technology then induces what’s called polarization, which is the process through which the skin forms. All layers of the skin regenerate – epidermis, dermis, appendages and even the hair that grows from the skin.

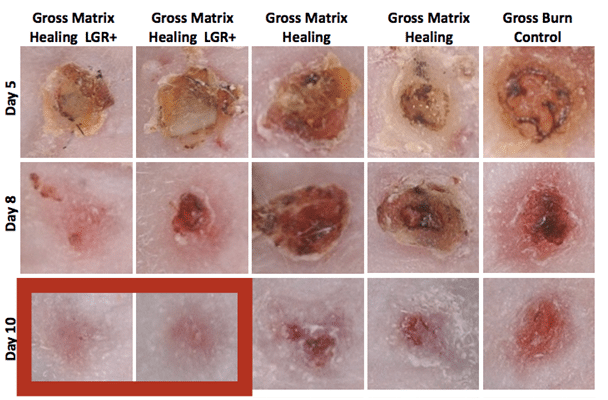

There are many applications for this technology, but the lead right now is wound recovery, and in particular, burn healing.

The image below shows the effect of SkinTE in a burn victim’s skin between 5 and 10 days after therapy.

Perhaps most importantly, the system is deployable with third-party scaffolds, which are basically support structures within which the skin grows, and these third party scaffolds are already FDA approved. This feature underpins a near to medium term investment thesis, rooted in the fact that it affords the company potential to partner with some of the bigger names in the space. Any such partnership would likely bring with it an injection of upfront capital, and – in turn – an upside revaluation.

What’s beyond SkinTE?

The technology that underpins SkinTE is applicable to a wide range of regeneration fields, and looking longer term, PolarityTE has plans to take advantage of this wide scope applicability. The company has already conducted studies of what it calls OsteTE, which is a bone regeneration technology, and AngioTE – a blood vessel regeneration platform.

To bring all this together, we’ve got a company that just took a quick route to market by way of a merger with Majesco, which has a technology in development that could completely revolutionize the way we treat burns. Beyond burns, bone regeneration, blood vessel regeneration, and more, are viable applications of the technology. Three big name investors are already involved, with a track record of backing succesful early stage biotech companies. There’s real potential for substantial upside revaluation near term on the back of partnership announcements, and longer term growth opportunities in the expanded scope of the platform.

It’s not risk free, of course. Biotechnology companies, and especially those at this end of the sector, often need to attract operational capital, and this will generally come at a cost of dilution to an existing base. The big returns are made by picking those for which the potential for growth outweighs the impact of dilution on an early exposure, and this looks to be one such opportunity.

Intercept Pharmaceuticals (NASDAQ:ICPT) Gilead Sciences, Inc (NASDAQ:GILD) Clovis Oncology, Inc. (NASDAQ:CLVS) Chiasma, Inc. (NASDAQ:CHMA)")

Might Be Moving Away From Its Initial Plan With Messenger")

Is Running Right Now")