- Negative Interest Rates, or NIRP for Negative Interest Rate Policy, are now the norm in the Eurozone, Switzerland, Denmark, and now Sweden

- NIRP essentially means that depositors pay money on their savings instead of earning a return

- This discourages savers from saving in cash, encouraging spending instead

- The aim is to jolt the economy by encouraging people to spend more sooner, increasing price inflation

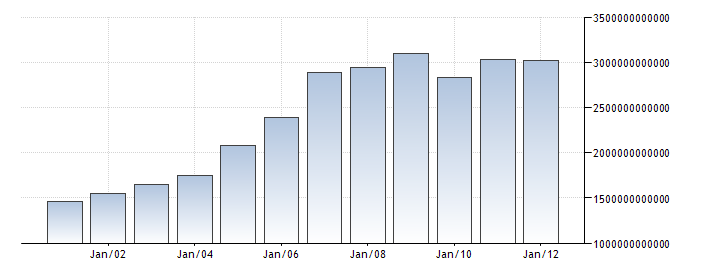

- Despite the effort, Sweden’s money supply has not increased substantially since 2007,

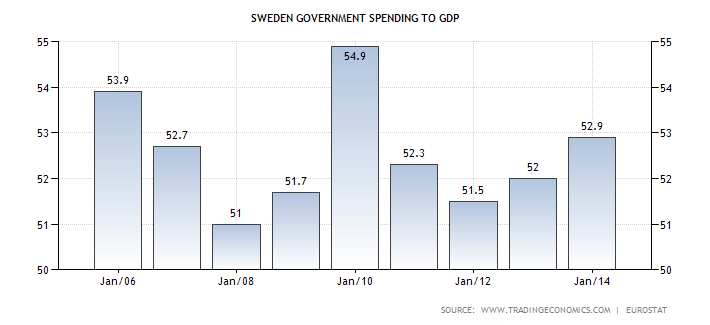

- Government spending has not increased relative to GDP either

Sweden’s Riksbank, the world’s oldest central bank founded in 1668, has for the first time in its 347-year history brought its benchmark interest rate to negative, -0.1% to be exact. Depositors at the Riksbank, consisting of other Swedish banks, now have to pay the central bank to store cash there. The effect of this will be to encourage Swedish banks not to store cash at the Riksbank since it now costs money to do so, but instead to loan it out to borrowers.

In addition to bringing its benchmark rate to -0.1%, the Riksbank has announced a trial balloon of 10 billion Krona (kr) in bond buying. While that only amounts to $1.2B, in combination with negative rates it is a very aggressive – and dangerous – money-printing strategy.

On the news, the Swedish Krona fell 1.5% against the US Dollar and the Euro.

Sweden now joins Switzerland, Denmark, and the entire Eurozone in charging depositors for their savings. For their respective governments with heavy debt loads, this is quite a boon because now if the Swedish government under -0.1% interest rates issues a bond for, say, 1000 Krona, it will only have to pay 990 back at maturity. In the twilight zone, this would be the ideal way to get out of debt – borrow yourself back to solvency with negative interest rates!

It works on paper, that is until the market overwhelms the irrationality of NIRP and people stop buying bonds altogether, forcing interest rates through the roof over the furor of central bank monetary policy.

Interestingly enough, Sweden’s money supply did not increase at all through the beginning of the financial crisis in 2008. Though the last available report was issued in 2012, Sweden’s money supply stood at 3 trillion krona from 2007 until 2012. This means Sweden, despite going into NIRP, has one of the tightest monetary policies in the world, at least until 2012. Go figure.

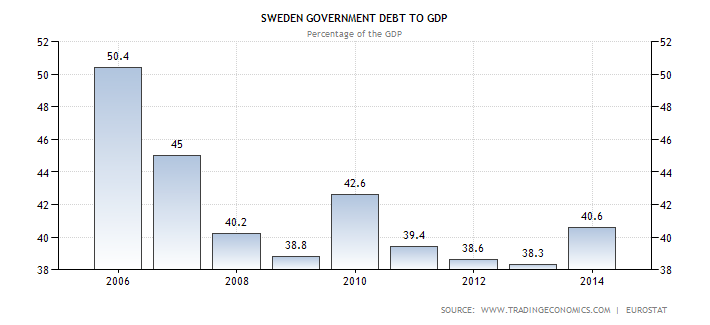

In addition to strangely having one of the tightest monetary policies – if not the tightest – in all of Europe, Swedish government debt is also quite low at just over 40% GDP.

Spending is also stable relative to GDP, and has fluctuated between 51% and 55% of GDP for nearly a decade.

Spending is also stable relative to GDP, and has fluctuated between 51% and 55% of GDP for nearly a decade.

Conclusion – while Sweden is now wading into NIRP, it still has one of the most conservative monetary and fiscal policies in the world.

Intercept Pharmaceuticals (NASDAQ:ICPT) Gilead Sciences, Inc (NASDAQ:GILD) Clovis Oncology, Inc. (NASDAQ:CLVS) Chiasma, Inc. (NASDAQ:CHMA)")

Might Be Moving Away From Its Initial Plan With Messenger")

Is Running Right Now")